The question that often arises in discussions about state-issued currencies is whether such initiatives, like those proposed in Kentucky or Ohio, are constitutional. They function as a form of currency that could serve as a pillar of stability for our nation, especially in an era where federal monetary policy has led to rampant inflation and economic uncertainty. I found myself pondering this deeply during a recent visit to the Ohio Statehouse, where I reconnected with old friends who work there. It was a serendipitous encounter that led me straight into the office of Senator George Lang, a man I’ve always admired for his sharp intellect and unwavering commitment to conservative principles. Lang and I have shared many conversations over the years, often diving into the world of books—recommendations that challenge the status quo and inspire action. On this particular day, as we caught up, the discussion turned to a topic that has been gaining traction among legislators and economic thinkers alike: a return to sound money through a state-level gold standard.

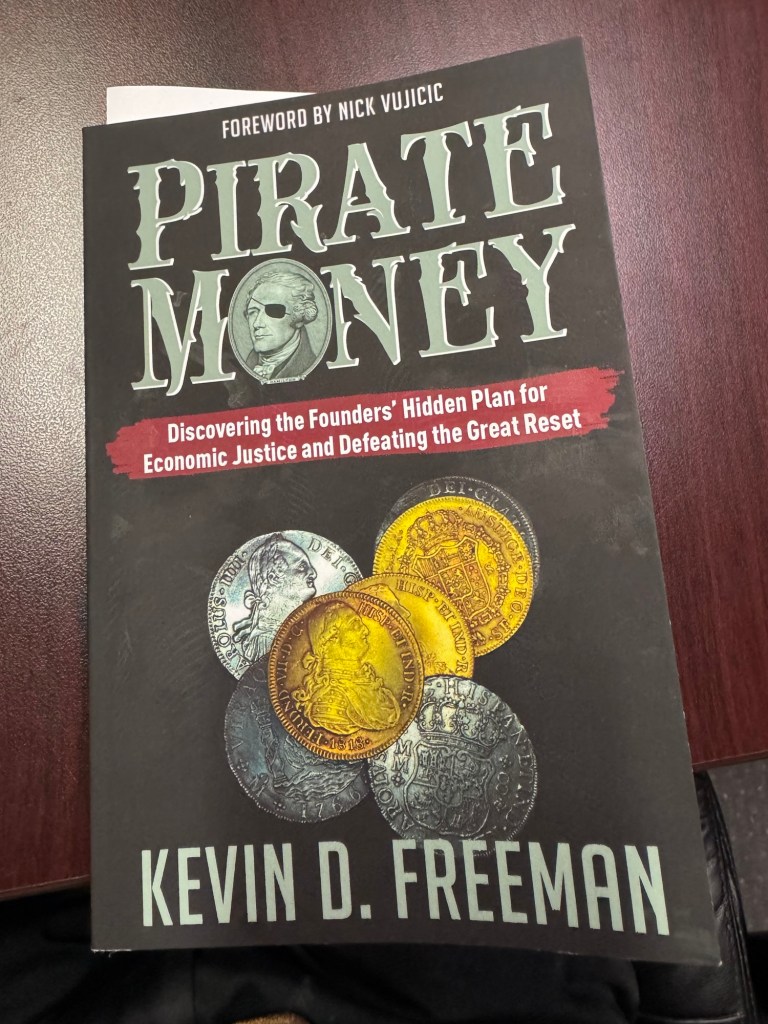

Lang handed me a copy of a relatively new book by Kevin Freeman, titled Pirate Money. The Blaze publishes it, and Freeman, whom I’ve followed through his economic commentary on that platform, draws from his extensive background advising the Pentagon and military leaders on financial warfare. I’ve known people at The Blaze over the years, and Freeman’s insights into global economics have always struck me as prescient. This book isn’t just another treatise on monetary policy; it’s a call to action, proposing an innovative way for states to reclaim control over their currencies using gold and silver, bypassing the Federal Reserve’s failures. As Lang and I talked, he mentioned that he’s been encouraging his colleagues in the legislature to read it by passing out copies from his office. The concept resonated with me immediately, especially after my own harrowing experiences with banks in 2025—a year that exposed the ugly underbelly of the financial industry in ways I hadn’t fully appreciated before.

You see, I’m not inherently anti-bank; they’ve served a purpose in facilitating commerce. But last year, I encountered the kind of predatory behavior that makes you question the entire system. Hidden fees, arbitrary account freezes, and a lack of transparency revealed the “ugly people” behind the polished facades—executives and regulators who prioritize control over service. This isn’t isolated; it’s symptomatic of a broader issue tied to the Federal Reserve and its monopoly on money creation. Freeman’s book delves into this, explaining how the Fed’s policies have enabled entities like BlackRock to amass unprecedented power, launder printed money through Wall Street, and impose agendas such as ESG (Environmental, Social, and Governance) criteria on corporations. If a CEO steps out of line, they risk deplatforming or worse—losing access to banking services based on social media profiles or political affiliations. I’ve seen this firsthand; banks now scrutinize applicants’ online presence, denying services to those deemed “undesirable.” This social credit system, imported from communist China, has infiltrated American finance, and it’s out of control.

My conversation with Lang covered a lot of ground, but the gold standard idea stood out. Freeman argues for a “constitutional backdoor” via Article 1, Section 10 of the U.S. Constitution, which prohibits states from coining money or emitting bills of credit but explicitly allows them to make “nothing but gold and silver coin a tender in payment of debts.” This clause, rooted in the Founders’ distrust of fiat currency following the inflationary disasters of the Continental Dollar during the Revolutionary War, grants states the authority to establish gold and silver as legal tender. Freeman’s proposal builds on this: states could create vaults where citizens deposit gold, which is then used as backing for a digital debit card system. You’d buy gold with dollars, store it in the state vault, and spend it via a card that deducts the equivalent value in real time, adjusted for market prices. No need to carry physical coins; it’s as convenient as swiping a credit card, but insulated from inflation.

This isn’t a pie-in-the-sky theory. Texas has already paved the way with its Texas Bullion Depository, established in 2015, a state-run facility for storing precious metals. In 2025, Texas advanced further with House Bill 1056, enabling gold and silver deposits to be spent via debit-style cards, creating a digital payments platform backed by physical bullion. By January 2026, the Texas Comptroller was seeking industry input on this system, aiming to implement it by May 2027 without state funding, relying instead on service fees. Ohio is following suit. In April 2025, Representatives Brian Lorenz, Mark Johnson, and Josh Williams sponsored House Bill 208 (though some records refer to similar legislation as HB 206, sponsored by Representative Jennifer Gross), which aims to establish a transactional currency based on gold and silver. The bill has been circulating but is currently stuck in the Judiciary Committee, needing leadership to push it forward. Lang and Gross are key supporters, with Lang distributing Freeman’s book to build momentum. This isn’t just for the wealthy; it’s a democratizing force that allows everyday people to protect their savings from erosion.

To understand why this is urgent, we must revisit the history of America’s monetary system—a tale of stability lost to central planning. In colonial America, currency was scarce and chaotic. The British Crown restricted silver and gold inflows to the colonies, forcing settlers to rely on foreign coins, barter, or makeshift scrip. The most common was the Spanish “piece of eight,” or eight-reales silver coin, minted in the New World and prized for its consistent value. Pirates played a surprising role here; they plundered Spanish galleons, circulating these coins throughout the Atlantic world. Freeman draws the title Pirate Money from this era, noting that “pirate money”—looted Spanish silver—fueled early American commerce by evading royal monopolies. These coins were often cut into “bits” for change—a one-reale bit equaled 12.5 cents, hence “two bits” for a quarter. This decentralized, metal-backed system contrasted sharply with the inflationary paper-money experiments, such as Massachusetts’ pine-tree shillings or the Continental Congress’s fiat notes, which collapsed under overprinting.

The Founders, scarred by hyperinflation during the Revolution—where “not worth a Continental” became a proverb—enshrined sound money in the Constitution. Congress was granted the power to “coin money” and regulate its value, while states were barred from issuing fiat currency but were allowed to accept gold and silver tender. The U.S. adopted a bimetallic standard in 1792, with the dollar defined as a specific weight of silver or gold. This stability propelled economic growth until the 20th century. But cracks appeared with the Civil War’s greenbacks, fiat notes that depreciated rapidly. Post-war, the U.S. returned to gold in 1879, enjoying decades of low inflation and prosperity.

The turning point came in 1913 with the Federal Reserve’s creation, ostensibly to stabilize banking, but it granted a private cartel monopoly over the money supply. Critics, including Freeman, argue this enabled endless printing, detached from real assets. Then, in 1933, amid the Great Depression, President Franklin D. Roosevelt issued Executive Order 6102, confiscating private gold holdings at $20.67 per ounce, only to revalue it at $35 shortly after via the Gold Reserve Act of 1934—a 69% devaluation that transferred wealth to the government. This severed the dollar’s domestic full gold backing, though international convertibility persisted under Bretton Woods.

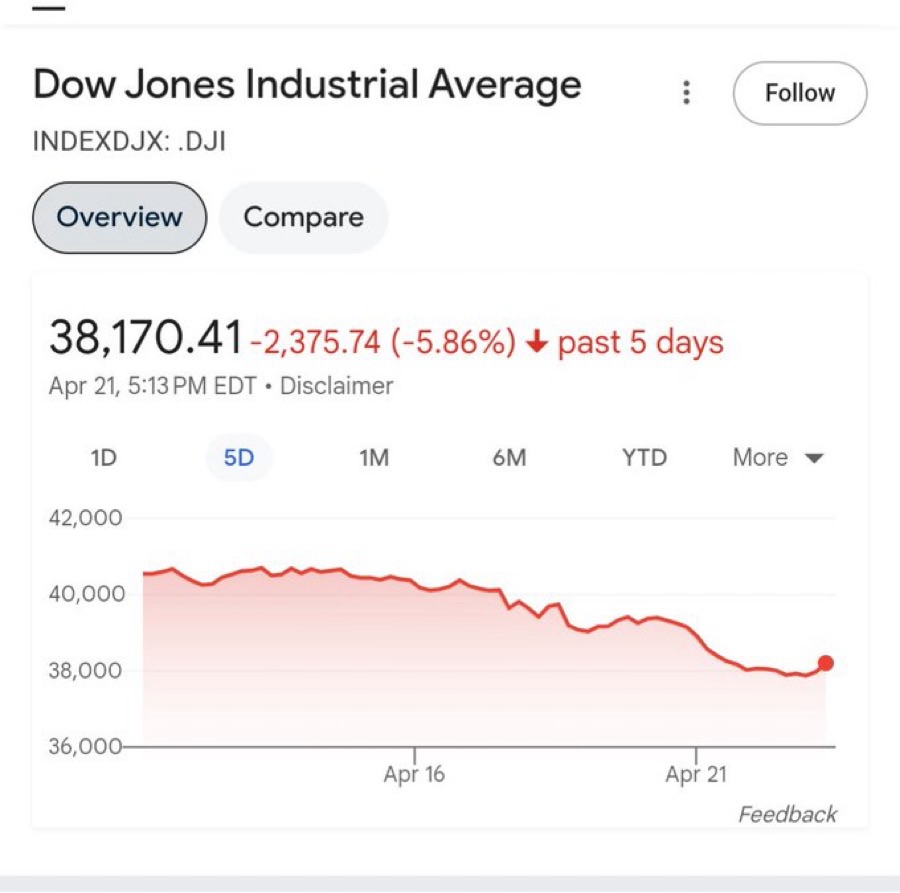

The final blow was the “Nixon Shock” in 1971. Facing gold outflows and inflation from Vietnam War spending, President Richard Nixon suspended dollar-to-gold convertibility on August 15, 1971, effectively ending the gold standard. This unleashed fiat money, where dollars are backed only by faith in the government. The results? Catastrophic inflation. In the 1970s, prices soared, with annual rates peaking at 15% in 1980. A dollar from 1970 buys just 13 cents worth of goods today—an 87% erosion. Over the last century, the dollar has lost over 96% of its purchasing power since 1913. From 1925 to 2025, it’s declined 95%, with stark generational impacts: $100 in 1975 is worth $16.40 today.

This inflation isn’t accidental; it’s baked into the system. The Fed targets 2% annual inflation, but real rates often exceed that target, especially post-2020, with COVID stimulus flooding trillions into the economy. Homes, once affordable on a single income, now price out young families. Everything’s too expensive because money loses value yearly. Freeman highlights the shift from a production economy—making stuff—to a finance economy, where wealth comes from trading paper assets, interest rates, and debt manipulation. BlackRock exemplifies this: managing trillions, it influences CEOs via asset control, pushing agendas that prioritize globalism over American interests. During the pandemic, the Fed hired BlackRock to manage bond purchases, raising conflict-of-interest concerns by blurring the lines between public policy and private profit.

Compounding this domestic rot are external threats. President Trump understood this, cracking down on Iran, Venezuela, Mexico, and Canada to protect the dollar from attacks. Why Greenland? Strategic resources. But the real adversary is China, propped up since Nixon’s 1972 visit, which opened the door to currency manipulation and intellectual property theft. Freeman, an expert in economic warfare, warns that wars today are fought through finance, not just bombs. China has been waging a stealth assault on the dollar: dumping U.S. Treasuries, stockpiling gold, and promoting the renminbi as a reserve currency. In 2026, Beijing issued directives for financial institutions to divest Treasuries en masse, spiking yields and straining U.S. debt financing. Allies like the BRICS nations follow suit, accelerating de-dollarization. If the dollar falls, America’s global clout crumbles—exactly China’s aim.

Trump provided a reprieve from 2017 to 2021, stabilizing the dollar amid these assaults. But with Democrats pushing centralized planning and Republicans sometimes complicit, the direction is toward more control. The Great Reset, championed by globalists, envisions a world where you “own nothing and be happy,” with currencies digitized for surveillance. Freeman’s Pirate Money counters this: states like Ohio and Texas can rebel by creating gold-backed systems, using the cashless infrastructure against the centralizers.

Imagine: You deposit your paycheck into an Ohio vault, converting it to gold at current prices. Your “black card” deducts value for purchases—gas, groceries, PlayStation—without inflation’s bite. Gold appreciates, so savings grow. No more losing 2-5% per year; your money retains value. This forces the Fed to compete, curbing excesses. It’s not Bitcoin’s volatility; it’s stable, tangible gold, recognized worldwide since antiquity.

Critics say it’s for the rich, but Freeman argues otherwise. Centralized bankers thrive on monopoly, leveraging inflation to steal value. By decentralizing, more people retain wealth, reducing inequality. In Ohio, HB 208 needs champions. Knock on Lang’s door; he’ll give you the book. Gross is sponsoring related efforts. With Vivek Ramaswamy as governor in Ohio and in partnership with a Trump administration, support could surge.

This isn’t radical; it’s constitutional. States have the right, and the time is now, while Trump stabilizes the dollar. Democrats should back it too—protecting value benefits all. If we wait, inflation will devour more. As Freeman notes, pirates used gold to win independence; we can too.

In conclusion, Kentucky’s notes—or any state’s gold tender—are constitutional under Article 1, Section 10. They stabilize our nation against Fed failures, BlackRock’s influence, and China’s attacks. Ohio, lead the way with HB 208. I’ll be one of the first to sign up.

Footnotes

1. U.S. Constitution, Article 1, Section 10: “No State shall… coin Money; emit Bills of Credit; make any Thing but gold and silver Coin a Tender in Payment of Debts…”

2. Kevin D. Freeman, Pirate Money (The Blaze, 2025), pp. 45-67, discussing colonial use of Spanish coins.

3. Executive Order 6102, April 5, 1933, by Franklin D. Roosevelt, requiring the surrender of gold at below-market rates.

4. Gold Reserve Act of 1934, revaluing gold from $20.67 to $35 per ounce.

5. Nixon Shock: Suspension of gold convertibility, August 15, 1971.

6. Inflation statistics: Dollar lost 87% value since the 1970s; peaked at 15% in 1980.

7. BlackRock’s role in Fed bond programs, 2020.

8. China’s Treasury divestment, 2026 directives.

9. Texas Bullion Depository, established 2015; HB 1056, 2025.

10. Ohio HB 206 (or 208 variant): Gold and silver transactional currency.

Bibliography

• Freeman, Kevin D. Pirate Money: The Constitutional Path to Sound Money. The Blaze, 2025.

• Griffin, G. Edward. The Creature from Jekyll Island: A Second Look at the Federal Reserve. American Media, 1994.

• Rothbard, Murray N. What Has Government Done to Our Money? Ludwig von Mises Institute, 1963.

• Eichengreen, Barry. Golden Fetters: The Gold Standard and the Great Depression, 1919-1939. Oxford University Press, 1992.

• Lowenstein, Roger. “The Nixon Shock.” Bloomberg Businessweek, August 4, 2011.

• U.S. Constitution, Annotated Edition. Library of Congress.

• Federal Reserve Economic Data (FRED). “Purchasing Power of the Consumer Dollar.”

• Texas Comptroller of Public Accounts. “Request for Information: Digital Payment System Backed by Bullion,” January 2026.

• Ohio House of Representatives. “H.B. No. 206: Establish a Transactional Currency Based on Gold and Silver.”

• Freeman, Kevin D. Advisory Reports to Pentagon on Economic Warfare, Various Dates.

Rich Hoffman

More about me

Click Here to Protect Yourself with Second Call Defense https://www.secondcalldefense.org/?affiliate=20707

About the Author: Rich Hoffman

Rich Hoffman is an independent writer, philosopher, political advisor, and strategist based in the Cincinnati/Middletown, Ohio area. Born in Hamilton, Ohio, he has worked professionally since age 12 in various roles, from manual labor to high-level executive positions in aerospace and related industries. Known as “The Tax-killer” for his activism against tax increases, Hoffman has authored books including The Symposium of Justice, The Gunfighter’s Guide to Business, and Tail of the Dragon, often exploring themes of freedom, individual will, and societal structures through a lens influenced by philosophy (e.g., Nietzschean overman concepts) and current events.

He publishes the blog The Overmanwarrior (overmanwarrior.wordpress.com), where he shares insights on politics, culture, history, and personal stories. Active on X as @overmanwarrior, Instagram, and YouTube, Hoffman frequently discusses space exploration, family values, and human potential. An avid fast-draw artist and family man, he emphasizes passing practical skills and intellectual curiosity to younger generations.